What if your insurance premium actually moved in sync with your business growth? Most entrepreneurs accept the traditional model of heavy down payments and year-end audit surprises as a necessary evil. It's time to reframe that thinking. By switching to pay-as-you-go workers compensation, you transform a rigid administrative burden into a flexible, strategic asset. This approach ensures you only pay for the coverage you need, exactly when you need it.

We understand that managing cash flow is the heartbeat of your operations. You shouldn't have to choose between protecting your employees and maintaining your liquidity. It's a stressful balancing act that often leads to inaccurate estimates and wasted time. This guide will show you how to leverage real-time payroll data to stabilize your monthly expenses and simplify your regulatory life. We'll explore how to eliminate large upfront costs, automate your compliance, and help you navigate the evolving rate landscape. As businesses nationwide look for smarter solutions, now is the perfect moment to prioritize your people while protecting your bottom line.

Key Takeaways

- Move from rigid annual estimates to a fluid, real-time premium model that preserves your business's vital cash flow.

- Discover how pay-as-you-go workers compensation leverages a direct data handshake with your payroll to calculate exact premiums per pay period.

- Turn the dreaded year-end audit from a source of financial stress into a routine, manageable verification process.

- Learn the five-step strategy for a seamless transition, ensuring your compliance remains automated and your coverage never lapses.

- See how a strategic partnership can unify your insurance, providing the organizational security and regional expertise your business deserves.

Understanding Pay-As-You-Go Workers' Compensation in 2026

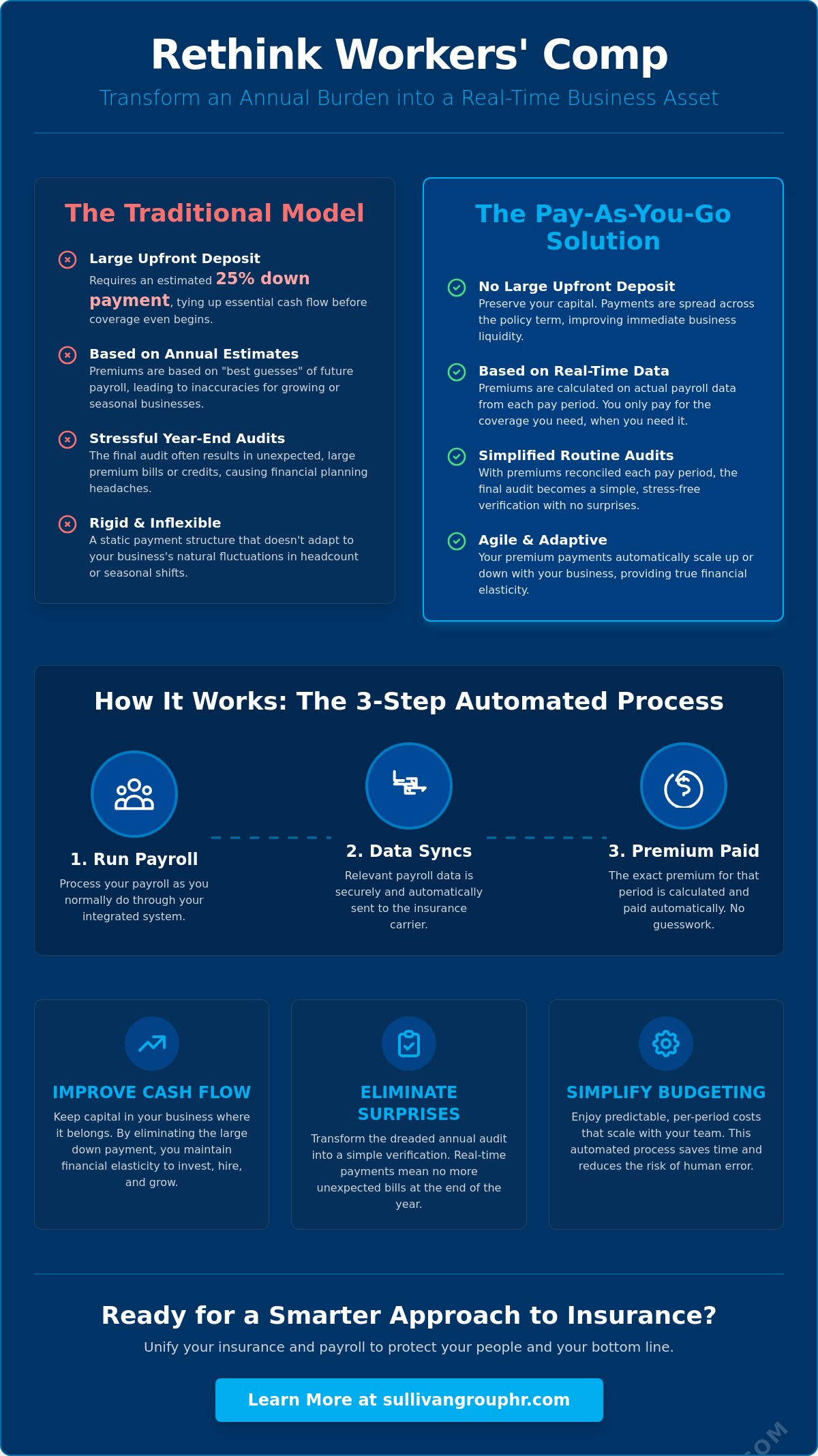

How much of your hard-earned capital is currently sitting idle in an insurance carrier's bank account? For many business owners, the answer is "too much." Traditional insurance models demand that you pay for yesterday's projections with today's liquid cash. It's a rigid, outdated approach that doesn't account for the speed of modern business. Pay-as-you-go workers compensation represents a fundamental shift in how you manage risk. It is a real-time premium calculation model that syncs directly with your actual payroll cycles. Instead of paying based on who you think you will hire, you pay based on who is actually on the clock right now.

As we move through 2026, the economic environment remains unpredictable. While the Florida Office of Insurance Regulation approved an average 6.9 percent rate decrease for new and renewal policies starting January 1, 2026, managing every dollar remains vital. This agile financial model serves businesses that experience seasonal shifts, rapid growth, or fluctuating headcounts. It replaces guesswork with granular accuracy. We see this as more than just a payment plan; it's a tool for organizational security that adapts as quickly as you do. Whether you are a local contractor or a growing tech firm, precision matters.

The Core Difference: Estimates vs. Reality

Traditional policies are built on a foundation of "best guesses." You project your annual payroll, the carrier calculates a premium, and you typically hand over a 25 percent down payment just to start the policy. It's a heavy lift before you've even covered a single shift. In contrast, the pay-as-you-go model utilizes a direct data handshake with your payroll administration software. There is no massive upfront deposit. There are no static annual projections. You get precision, protection, and a payment schedule that mirrors your actual liabilities. It's a smarter way to stay compliant without the heavy entry fee.

Why Cash Flow is Your Competitive Advantage

Think about the opportunity cost of that 25 percent down payment. That capital could be funding your next applicant tracking system upgrade, driving your R&D efforts, or bolstering your cash reserves. We call this "financial elasticity." By keeping your capital liquid, you maintain the freedom to pivot when the market shifts. This model offers three distinct benefits to your bottom line:

- Immediate liquidity: Keep your cash in your business where it can generate a return.

- Simplified budgeting: Enjoy predictable per-period costs that scale with your team size.

- Reduced friction: Eliminate the need for large, lump-sum payments that disrupt your monthly planning.

By integrating your workers' compensation insurance into your broader human capital management strategy, you create a seamless flow of data and dollars. This isn't just about insurance; it's about building a stable foundation for your professional potential. Why tie up your future in a legacy payment model when you can pay for exactly what you use?

The Mechanics: How Real-Time Payroll Integration Drives Accuracy

How do you turn a complex regulatory requirement into a silent background process? The answer lies in the digital handshake between your payroll administration and your insurance carrier. This connection ensures that every time you click "submit" on your payroll, the exact premium for that period is calculated and prepared. It’s the definition of precision. By syncing these two systems, you eliminate the friction that usually defines the relationship between a business and its insurer.

Pay-as-you-go workers compensation removes the guesswork that plagues traditional models. Instead of a manual upload or a quarterly report, the system pulls data directly from your verified payroll records. This automated withdrawal aligns perfectly with your schedule. It saves your accounting team hours of tedious reconciliation. It protects your business from the human error that often leads to costly penalties. When your insurance payments mirror your actual payroll, your financial records remain clean and predictable.

The Role of Class Codes and Rate Precision

Accuracy depends on more than just the total payroll amount. It depends on who is doing the work. A class code is a four-digit numerical code used by insurance companies to categorize work. For example, a clerical worker carries a different risk profile than a construction site supervisor. If you hire a new team member mid-year, a traditional plan might misclassify them until the next audit. Real-time reporting ensures that class codes are applied correctly per pay period. This prevents expensive misclassification errors before they can snowball into a major liability.

Seamless Data Flow through HCM Platforms

Why manage two separate silos when you can use one unified system? Utilizing a platform like isolved creates a single source of truth for your human capital management. By removing manual data entry, you eliminate the primary cause of audit discrepancies. This is the "set-it-and-forget-it" advantage of modern systems. Your data stays clean, your premiums stay accurate, and your team stays focused on growth. We believe that your time is too valuable to spend on administrative friction. When your systems work together, you create a more resilient organization. If you’re ready to streamline your operations, exploring integrated payroll and insurance solutions is the logical next step. It’s about working smarter, not harder.

Traditional vs. Pay-As-You-Go: Solving the 'Audit Surprise' Problem

Does the thought of your annual insurance review keep you up at night? For many business owners, the year-end audit is a source of intense financial stress. It’s the moment when your "best guesses" from twelve months ago finally meet reality. In a traditional model, this often leads to a massive "Catch-Up Payment" that can cripple your quarterly budget. By contrast, pay-as-you-go workers compensation replaces this anxiety with transparency. You move from a reactive posture to a proactive one. Instead of a surprise bill, you experience a simple "True-Up" that confirms what you already know. It’s about clarity, precision, and peace of mind.

We believe that your insurance should be a safety net, not a source of administrative dread. The traditional "estimate-and-adjust" model is fundamentally flawed because it assumes your business is static. But you are growing, pivoting, and evolving. When your payment model is rigid, you lose the ability to manage your cash flow effectively. By utilizing real-time data, you create a digital paper trail that lasts all year. This transparency protects you from the sudden, large-scale financial hits that often follow a manual audit. You deserve a system that works as hard as you do.

The 'Audit Trap': Why Estimates Often Fail

Traditional insurance is built on static projections. If your business grows 20 percent mid-year, your original estimate becomes obsolete within months. You end up owing a significant balance at the end of the term. Conversely, if you experience a slowdown or layoffs, the insurer holds onto your overpaid premiums for months before issuing a refund. Your money is effectively trapped. This is the "Audit Trap." It penalizes your success and ignores your struggles. Real-time data ensures that your payments fluctuate alongside your payroll, keeping your capital exactly where it belongs: in your operating account.

Streamlining the Annual Review Process

There is a common misconception that pay-as-you-go prevents audits entirely. It doesn't. However, it does transform the process from a forensic investigation into a routine verification. Carriers trust real-time data more than manual year-end summaries because the digital paper trail is established in every pay cycle. You aren't scrambling to find missing documents or explain classification changes. For a deeper look at protecting your business, explore our guide on HR risk management. When your workers' compensation insurance is integrated into your human capital management, the audit becomes a non-event. It’s just another day at the office.

Strategic Implementation: Transitioning Your Business to a Pay-As-You-Go Model

Are you ready to stop overpaying for insurance you haven't used yet? Moving away from a traditional model requires a deliberate plan. It is not just a change in how you write checks. It is a structural upgrade to your financial operations. Transitioning to pay-as-you-go workers compensation works best when you follow a clear roadmap. This ensures that your coverage remains continuous while your cash flow becomes fluid. We recommend a five-step process: assess your renewal date, gather historical data, integrate your systems, cancel the legacy policy, and finalize the outgoing audit.

Timing is everything. While you can switch at any time, the policy renewal date is the ideal moment. It eliminates the risk of short-rate cancellation penalties from your current carrier. It also provides a clean break for your accounting records. To start, you will need your current class codes, recent loss runs, and a detailed payroll journal. This documentation serves as the foundation for your new, more accurate system. Handling the final audit of your old policy is the last hurdle. Since you are moving to a real-time model, this will be the last time you face a major "catch-up" bill. It is the final step toward long-term organizational security.

Evaluating Your Current Payroll and Insurance Silos

Does your current provider actually support a direct data handshake? Not all systems are created equal. Some require manual uploads that defeat the purpose of automation. Before you make the switch, ensure your human capital management platform is compatible with your carrier. You need clean, updated employee records to prevent "garbage in, garbage out" scenarios. We suggest choosing a partner that offers both high-level HCM technology and deep workers' compensation insurance expertise. This unified approach removes the friction between your HR and accounting departments.

Setting Up the Automated Workflow

Precision begins with mapping. You must align your payroll class codes with specific insurance requirements. This ensures every dollar is categorized correctly from day one. We always recommend a testing phase during the first pay cycle to verify that the math is perfect. During your first 90 days, keep a close eye on your premium withdrawals. Check for classification accuracy, monitor for new hire integration, and verify that your cash flow matches your expectations. If you are looking for a partner to guide you through this transition, contact our team today to discuss a tailored implementation plan. It is time to make your insurance work for you.

The Sullivan Advantage: Unifying Risk Management through isolved

Why settle for a transactional vendor when you can have a dedicated coach? Most insurance providers sell you a policy and vanish until your renewal date. We take a different path. By embedding pay-as-you-go workers compensation into the isolved platform, we create a single source of truth for your organizational data. This ensures your payroll administration, tax filings, and insurance premiums stay in perfect sync. It is a comprehensive human capital management strategy that protects your liquid capital while securing your team's future.

Our team at Sullivan Group HR understands the specific nuances of the local territory. We know that as of January 1, 2026, the Florida maximum weekly compensation rate rose to $1,358. Staying on top of these shifting regulations is what we do. We act as your advocate, analyzing your risk profile to find efficiencies that automated systems often miss. By unifying your risk management, you move away from administrative friction and toward a partnership built on stability and results. It is a smarter way to lead.

Beyond Software: The Human Element of Risk

We bring a legacy of hard-earned wisdom to every client relationship. While technology provides the data, our experts provide the strategy. Sullivan Group HR serves as a supportive, no-nonsense authority in high-stakes environments. We offer proactive safety consulting to identify hazards before they turn into costly claims. This hands-on approach reduces your long-term costs and strengthens your professional potential. Unlike tech-only firms, we prioritize interpersonal value over automated processes. We value people over systems because your success is our primary metric.

Your Future-Proofed Workforce

Imagine a business where cash flow is fluid, compliance is silent, and talent is thriving. This is the reality of a unified risk management model. When your workers' compensation insurance lives within your broader HCM ecosystem, you eliminate the silos that cause financial stress. You gain the financial elasticity needed to invest in new opportunities or R&D. Are you ready to experience the security that comes with integrated protection? We invite you to secure your organization's future today. Contact us for a risk management consultation and let's strengthen your business's financial health together.

Strengthening Your Business Foundation for 2026

Are you ready to reclaim your capital and simplify your regulatory life? Transitioning to pay-as-you-go workers compensation is more than a simple financial adjustment. It is a commitment to precision, protection, and organizational security. By aligning your premiums with your actual payroll cycles, you eliminate the stress of year-end audits and unpredictable cash flow hits. You gain a clear, digital paper trail that protects your bottom line while you focus on your professional potential.

We bring over 25 years of hard-earned wisdom and regional expertise to your risk management strategy. By leveraging the industry-leading isolved HCM platform, we provide a single source of truth for your business data. Our comprehensive safety consulting and proactive advocacy ensure that your workforce remains protected and your costs stay manageable. Don't let outdated administrative burdens hold your growth back. Secure your cash flow and protect your team with Sullivan Group HR’s integrated workers' comp solutions today. We are here to act as your coach and ally in building a resilient, future-proofed business. Your success is our primary metric.

Frequently Asked Questions

Is pay-as-you-go workers' compensation more expensive than traditional insurance?

No, the base rates for your insurance are identical to those found in traditional plans. You're paying the same premium per hundred dollars of payroll; you're simply spreading those payments out across the year. This model eliminates the massive upfront deposit that often strains small business budgets. It ensures your costs align perfectly with your actual labor usage, preventing you from overpaying during slow months.

Does pay-as-you-go eliminate the need for an annual workers' comp audit?

No, carriers still perform an annual audit to verify the accuracy of your reporting. However, because your payroll data was uploaded in real-time throughout the year, the process is much faster and less intrusive. You've already built a digital paper trail with every pay cycle. This significantly reduces the risk of a large "catch-up" bill or a stressful forensic investigation at the end of the policy term.

Can I switch to a pay-as-you-go model in the middle of my policy year?

Yes, you can transition at any time, though the policy renewal date is often the cleanest break for your accounting records. Switching mid-year may require your current carrier to perform a short-term audit to close out the previous plan. We recommend coordinating with your payroll provider to ensure the data handshake is ready before you cancel your existing coverage. This proactive approach prevents any gaps in your protection.

What happens if I have a pay period with zero payroll?

You owe zero premium for that specific period. Since pay-as-you-go workers compensation is based on actual wages paid, no payroll means no insurance cost for that cycle. This is a massive advantage for seasonal businesses or contractors with fluctuating project schedules. Your expenses naturally contract when your activity slows down, preserving your vital cash flow when your business needs it most.

Do I need a specific payroll software to use pay-as-you-go workers' comp?

You need a payroll system that supports a direct, secure integration with your insurance carrier. Modern human capital management platforms like isolved are designed specifically for this purpose. They automate the data transfer, removing the need for manual uploads or messy spreadsheets. If your current software doesn't offer this connection, you may find yourself stuck with the administrative friction and inaccuracies of the traditional model.

How does pay-as-you-go affect my Experience Modifier (MOD) score?

The payment model itself doesn't change your MOD score calculation. Your score is still based on your historical claims and safety record compared to industry averages. However, having real-time visibility into your payroll and class codes helps you manage your risk more effectively. Better data leads to better safety decisions, which eventually lowers your premiums through an improved MOD score and safer workplace culture.

What are the common pitfalls to avoid when setting up pay-as-you-go?

The most common pitfalls include misclassifying employees and failing to update payroll records. If a worker is assigned the wrong class code, your real-time payments will be inaccurate from the start. You should also ensure your payroll administration and insurance systems are properly synced before the first run. Regular communication with your HR consultant helps identify these issues before they turn into expensive audit surprises at year-end.

Can small businesses with only one or two employees use this model?

Yes, this model is particularly beneficial for small businesses and startups. Since you don't have to pay a large down payment, you can keep your limited capital working within your operations. Even with just one or two employees, the administrative time you save on reporting and audits is significant. Pay-as-you-go workers compensation provides the same high-level organizational security that larger firms enjoy without the heavy financial entry fee.